by Dave Akers, IHSA

“A recession is when a neighbor loses his job. A depression is when you lose yours.” — Ronald Reagan

The ocean shipping industry is currently navigating a significant crisis as of March 2026, primarily driven by escalating geopolitical tensions in the Middle East. These disruptions have forced carriers to implement Emergency Fuel Surcharges (EFS) to offset skyrocketing bunker costs and operational inefficiencies.

The bunker fuel situation in Asia is already affecting transpacific ocean carriers as of late March 2026, with impacts expected to intensify within the next 30 days.

Following the effective closure of the Strait of Hormuz on February 28, 2026, bunker prices in key Asian hubs like Singapore have more than doubled, surpassing $1,000 per metric ton for low-sulfur fuel.

Immediate and Near-Term Impacts

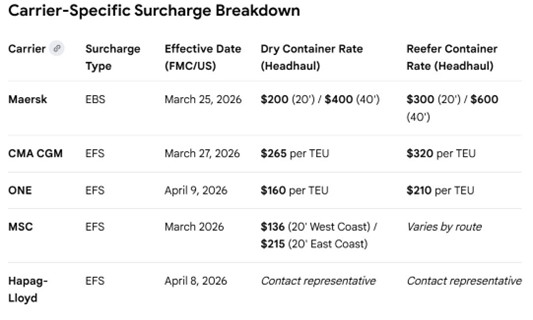

- Emergency Surcharges (Immediate): Major carriers including Maersk, MSC, ONE and CMA CGM have already introduced emergency fuel surcharges as of early March 2026. Maersk, for instance, implemented a global Emergency Bunker Surcharge (EBS) ranging from $200 to $400 for dry containers.

- Freight Rate Increases (Immediate to 30 Days): Spot rates from Shanghai to the U.S. West Coast rose tremendously in the third week of March, with analysts expecting further increases as fuel costs are passed on “almost immediately” or with a maximum 30-day notice to shippers.

- Operational Delays (Current): Refueling struggles at major ports like Singapore, Shanghai, and Ningbo-Zhoushan are leading to longer waits and increased port congestion. Some vessels are already detouring south to Singapore because of critical stock shortages in South Korea and China.

Regional Supply Outlook

The severity of the impact varies by location across the Asian network:

- Japan & South Korea: Facing “structural tightening” as governments prioritize domestic power grids over international vessel needs. Japan has already begun releasing state oil reserves to stabilize its market.

- China: A reported immediate ban on refined fuel exports was imposed in March 2026 to prevent domestic shortages, further squeezing regional bunker availability.

- Singapore: Remains the primary refilling point but is experiencing record-high premiums and increased “quality risk” due to forced fuel blending.

For every ship in a typical 35-day Los Angeles–Asia rotation, these fuel price hikes represent approximately $2 million in additional costs.

Key Operational Details

- Review Frequency: Maersk has stated they will review these levels every 14 days, adjusting them based on fuel availability and “mix”.

- Regulatory Phasing: Under Federal Maritime Commission (FMC) rules, carriers must typically provide 30 days’ notice for rate increases on U.S. trades. While global non-FMC trades saw these surcharges as early as March 2, the “gate-in” date for U.S. cargo remains the critical factor for April implementation.

- Backhaul Discounts: For return trips (U.S. to Asia), surcharges are generally 50% lower. For example, Maersk’s backhaul EBS is $100 for a 20-foot container.While both Transpacific Eastbound and Asia-Europe regions are experiencing emergency surcharges due to the March 2026 fuel crisis, Asia-Europe shippers are facing a much higher total cost burden. This disparity is driven by the fact that Asia-Europe vessels must now circumnavigate Africa via the Cape of Good Hope, significantly increasing fuel consumption and operational time compared to the more direct transpacific route.

Key Differences in Regional Impact

- Routing Inefficiency:Asia-Europe trade is currently defined by “embedded inefficiencies” as 100% of the fleet is forced around the Cape of Good Hope, absorbing market overcapacity but tripling fuel needs for that leg. Transpacific lanes remain physically insulated from these detours, but these costs will increase Asia to U.S. East Coast ports possible forcing more on the Transpacific.

- Price Volatility: Asia-Europe spot rates have seen “violent” spikes (up to 19% in a single week for Shanghai-Rotterdam) as carriers struggle to adjust. Transpacific rate hikes are described as “modest seasonal” increases by comparison.

- Fuel Availability: While both routes pull from Singapore’s tightening supply, Asia-Europe vessels require significantly more bunker fuel per voyage to complete the longer southern detour, making them more vulnerable to the current $1,000+ per ton price point.

- Inventory Strategies:U.S. importers are currently in a “waiting game” with high inventories, which has somewhat muted transpacific demand and kept rates from climbing as aggressively as the Europe lanes, where demand remains steadier.

These developments arrive as the industry navigates the 2026 – 2027 contract season, a period already marked by heightened volatility and cautious negotiations. As market conditions shift daily, staying informed on regional fuel availability and regulatory timelines will be essential for all stakeholders looking to mitigate the impact of this global maritime disruption. To help manage these complexities, let the International Housewares Shippers Association help you navigate contract negotiations and provide the clarity needed in this shifting landscape.

About IHSA

Don’t miss out on the significant savings available exclusively to IHA members through your shipper community, the IHSA. From May through April, members save millions on ocean freight costs.

Take advantage of this valuable resource today! Visit the International Housewares Shippers Association website or email team@shippersassociation.org to learn more and start saving.